The smart Trick of Mortgage Investment Corporation That Nobody is Talking About

Table of ContentsThe Best Guide To Mortgage Investment CorporationMortgage Investment Corporation Things To Know Before You BuyNot known Facts About Mortgage Investment CorporationGetting My Mortgage Investment Corporation To WorkMortgage Investment Corporation for Beginners

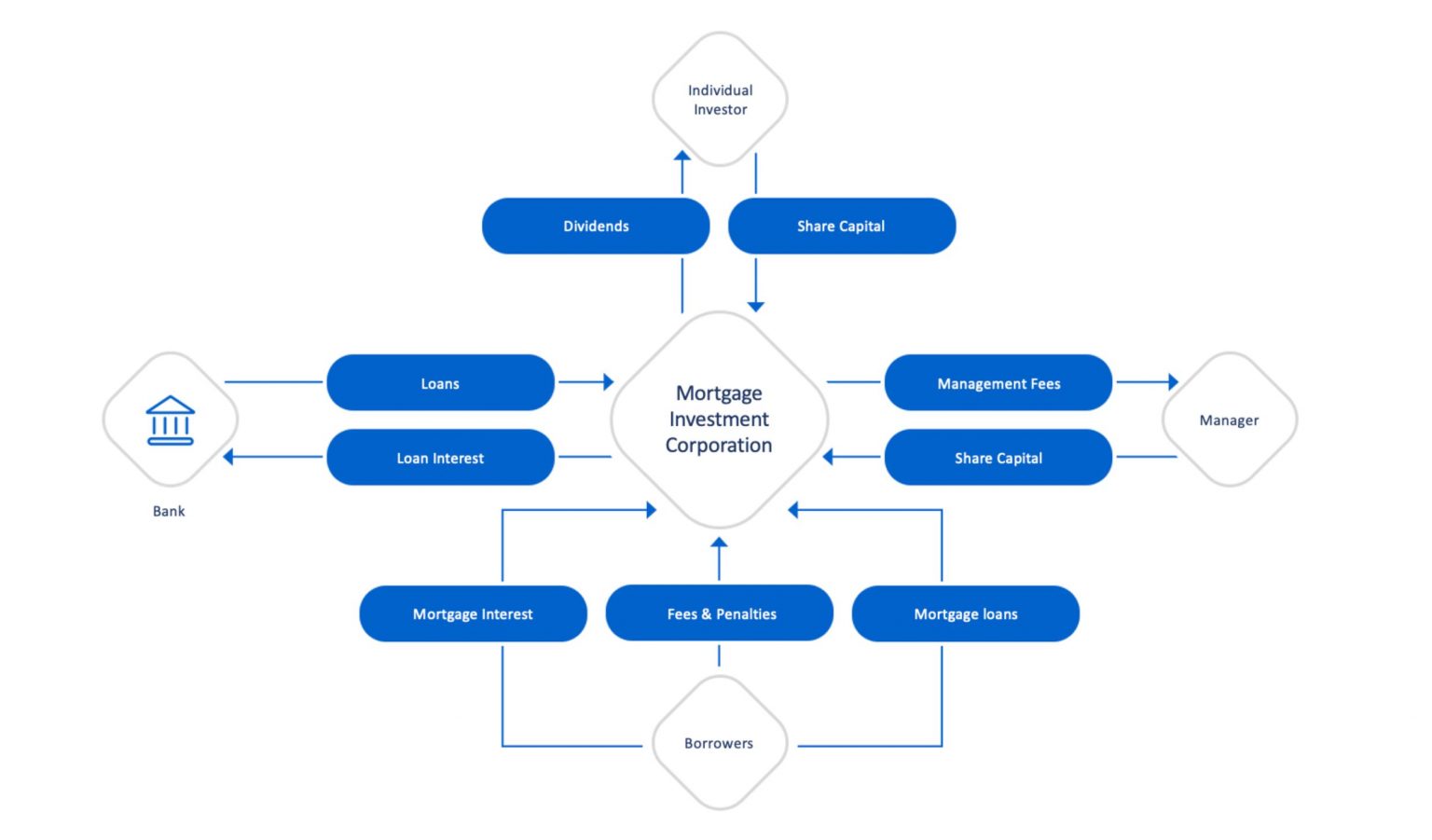

Does the MICs credit board evaluation each mortgage? In most scenarios, home mortgage brokers manage MICs. The broker should not serve as a member of the debt board, as this places him/her in a straight conflict of interest given that brokers usually earn a commission for placing the mortgages. 3. Do the directors, members of credit history committee and fund manager have their own funds invested? Although a yes to this question does not provide a safe financial investment, it needs to give some raised security if assessed along with various other sensible financing policies.Is the MIC levered? The monetary establishment will approve particular home loans possessed by the MIC as security for a line of debt.

Our Mortgage Investment Corporation Diaries

Last updated: Upgraded 14, 2018 Few investments couple of financial investments advantageous as a Mortgage Investment Home loan (Company), when it comes to returns and tax benefitsTax obligation Due to the fact that of their company structure, MICs do not pay income tax and are legally mandated to distribute all of their incomes to financiers.

This does not indicate there are not threats, yet, usually talking, no issue what the more comprehensive supply market is doing, the Canadian property market, especially significant urban areas like Toronto, Vancouver, and Montreal carries out well. A MIC is a company developed under the guidelines set out in the Earnings Tax Act, Section 130.1.

The MIC gains revenue from those home mortgages on passion costs and basic charges. The real appeal of a Mortgage Investment Firm is the return it supplies capitalists contrasted to various other fixed revenue financial investments - Mortgage Investment Corporation. You will have no trouble finding a GIC that pays 2% for a 1 year term, as federal government bonds are equally as low

Mortgage Investment Corporation Fundamentals Explained

There are strict needs under the Earnings Tax Obligation Act that a company must satisfy before it certifies as a MIC. A MIC must be a Canadian company and it must spend its funds in home loans. MICs are not permitted to handle or create real estate building. That said, there are times when the MIC finishes up possessing the mortgaged home as a result of foreclosure, sale contract, and so on.

MICs issue usual and preferred shares, releasing redeemable preferred shares to investors with a fixed returns rate. In many cases, these shares are thought about to be "certified investments" for deferred revenue plans. Mortgage Investment Corporation. This is excellent for capitalists who purchase Home mortgage Investment Firm shares via a self-directed registered retired life cost savings strategy (RRSP), signed up retirement earnings fund (RRIF), tax-free financial Click Here savings account (TFSA), deferred profit-sharing plan (DPSP), registered education and learning financial savings plan (RESP), or registered handicap savings plan (RDSP)

What Does Mortgage Investment Corporation Do?

And Deferred Strategies do not pay any type of tax on the rate of interest they are estimated to get. That stated, those who hold TFSAs and annuitants of RRSPs or RRIFs may be struck with particular fine tax obligations if the financial investment in the MIC is taken into consideration to be a "banned financial investment" according to copyright's tax obligation code.

They will certainly guarantee you have actually located a Mortgage Investment Corporation with "competent investment" condition. If the MIC qualifies, maybe extremely valuable come tax obligation time since the MIC does not pay tax on the rate of interest income and neither does the Deferred Plan. More broadly, if the MIC fails to meet the needs set out by the Earnings Tax Obligation Act, the MICs revenue will certainly be strained prior to it obtains distributed to shareholders, lowering returns considerably.

Many of these risks can be minimized however by speaking to a tax obligation expert and investment agent. FBC has worked exclusively with Canadian small company proprietors, entrepreneurs, investors, ranch operators, and independent specialists for over 65 years. Over that time, we have aided 10s of countless customers from throughout the country prepare and file their tax obligations.

The Ultimate Guide To Mortgage Investment Corporation

It shows up both the realty and securities market in copyright go to all time highs At the same time yields on bonds and GICs are still near document lows. Also cash is shedding its appeal since energy and food prices have actually pushed the inflation price to a multi-year high. Which begs the inquiry: Where can we still find value? Well I think I have the solution! In May I blogged regarding checking into mortgage financial investment corporations.

If rate of interest prices rise, a MIC's return would certainly additionally increase since greater home mortgage prices mean more revenue! Individuals that buy a mortgage investment company do not possess the property. MIC investors simply generate income from the enviable setting of investigate this site being a lending institution! It resembles peer to peer lending in the U.S., Estonia, or other parts of Europe, other than every loan in a MIC is secured by real estate.

Several tough working Canadians that want to purchase a residence can not get home mortgages from traditional financial institutions because possibly they're self utilized, or don't have a recognized credit scores history. Or possibly they want a short term loan to create a big home or make some remodellings. Financial institutions have a tendency to disregard these potential borrowers due to the fact that self utilized Canadians do not have steady incomes.